{{item.videoDuration}}

{{item.title}}

{{item.videoDuration}}

Seizing growth opportunities

India’s entertainment and media (E&M) sector is rapidly expanding, driven by its large millennial and Gen Z population of over 91 crore. The key enablers include 80 crore broadband subscriptions, 55 crore smartphone users, 78 crore internet users, rising per capita income, and the world’s cheapest data costs. Despite contributing less than 2% to the global E&M sector, India is the fastest-growing territory, supported by its expanding economy and technological infrastructure. Valued at INR 245k crore in 2023, the sector is projected to reach IN 345k crore by 2028, with a compound annual growth rate (CAGR) of 8.3%. Advertisement and connectivity is driving the growth in the sector. Mobile-first dominance in India is very significant, with Indians spending 82% of their time on E&M apps. Digital media, over the top (OTT), online gaming, animation and visual effects (VFX), live events and music are high-growth areas, with average CAGRs exceeding 15%. The Indian startup ecosystem and favourable government policies around foreign direct investment (FDI) further support domestic E&M growth.

Global E&M revenue (INR thousand crore) vs annual growth (%), 2019–2028

Manpreet Singh Ahuja, Chief Digital Officer and TMT Leader at PwC India

Total E&M revenue (excluding connectivity) in 2028 (INR thousand crore) and 2023–2028 CAGR (%)

Advertising will grow at a 9.4% CAGR from INR 101k crore in 2023 to INR 158k in 2028.

The share of advertising revenues will be consistent at ~20% during the period, while share of connectivity is estimated to increase from 52% to 56%, lowering the contribution of consumer revenues.

Connectivity revenues include fixed voice, fixed broadband access and value-added services, as well as mobile service revenue. Connectivity revenue totaled INR 263k crore in 2023, or 52% of the total Indian E&M revenue. It will reach INR 459k in 2028.

TV will remain the highest contributor to E&M revenues during the period; however, its share will drop from 43% to 36%.

Internet advertising is the second largest component with a share of 16%, which will increase to 21% by 2028.

Newspapers will continue to have a muted growth at 3.4%. Revenues are expected to increase from INR 38k crore in 2023 to INR 45k crore in 2028.

OTT is the third fastest growing segment with a CAGR of 14.9%.

India, fastest rising and declining E&M metrics by 2023–2028 CAGR (%)

Traditional TV Advertising revenues 2023 to 2028 in 2028 (INR thousand crore) & CAGR (%)

Newspaper & Magazines advertising revenues 2023 to 2028 in 2028 (INR thousand crore) & CAGR (%)

Internet advertising market in India – 2019–2028(e) (INR thousand crore)

Internet Advertising Revenue split by type, 2019–2028 (INR Cr in 000’s)

The proposed Digital India Act, replacing the Information Technology Act of 2000, aims to regulate the online advertising market to prevent dominance by a few big tech firms. By adhering to the DPDP Act, marketers can foster trust and transparency with consumers, leading to stronger relationships and more effective, personalised marketing campaigns. Restrictions on third-party data create opportunities for first-party data collection, resulting in more accurate data and better-targeted marketing. While the DPDP Act presents challenges, it also offers opportunities for innovation, trust-building and more effective marketing strategies. Brands that prioritise compliance will likely benefit from stronger customer relationships and a competitive edge.

TV market in India – 2023–2028(e) (INR thousand crore)

Number of households with TVs in India – 2023–2028(e), crore

OTT market in India – 2019–2028(e) (INR thousand crore)

OTT market in India – 2019–2028(e) (INR thousand crore)

OTT revenues split India 2023

Newspaper market: India has the second-fastest-growing newspaper market in the world after Pakistan. It is one of the markets that continues to grow contrary to the global decline in this segment.

Book market in India – 2023–2028(e), INR thousand crore

Book market: India leads the Asia Pacific region with a rapid increase in consumer book market revenue.

Online gaming market in India – 2023–2028(e) (INR thousand crore)

E-sports market in India – 2023–2028(e), INR Crore

India video games and esports revenue split by market share Revenue (INR thousand crore), 2023-28

India casual gaming revenue split (INR Cr 000’s), 2019-2028

Music sector: India’s recorded music industry is experiencing rapid growth as smartphone users increasingly seek out content through legitimate licensed music apps.

Podcast sector: There were 15.3 crore monthly podcast listeners in India in 2023.

Radio sector: Given the size of its population, India’s radio market remains relatively underdeveloped compared with other countries, leaving it much room for expansion.

Music sector in India – 2019–2028(e) (INR thousand crore)

Music subscribers in India – 2019–2028(e) (in crore)

Podcast ad revenue in India – 2019–2028(e) (INR crore)

Monthly podcast listeners in India – 2019–2028(e) (in crore)

Radio ads revenue in India – 2019-2028(e) (INR thousand crore)

OOH market in India – 2019–2028(e) (INR thousand crore)

OOH market segment – 2023

Cinema market in India – 2019–2028(e) (INR thousand crore)

In 2023, total B2B revenue grew by 9.2% to reach INR 8,465 crore, led by the continued recovery of the trade shows vertical. It is expected to grow at a 5.6% CAGR, reaching INR 11,142 crore by 2028 with highest growth pace in the world.

Business information: The vast size of India’s consumer market ensures high demand for business information, and the largest global market research firms have recognised this.

The business information market in India was valued at INR 5,301 crore in 2023 after growing by 4.0% y-o-y and it is expected to grow at a 4.5% CAGR, reaching INR 6,601 crore by 2028.

B2B market in India 2019–2028(e), INR thousand crore

Market research firms are aligning themselves with a broader trend towards integrated data analysis, combining survey data, client data and social data to gain a comprehensive understanding of consumer behaviour and market trends.

Custom research and analytics is fuelling growth in the country’s market research sector.

Trade shows: Trade shows represented 34.3% of India’s B2B market in 2023. They are expected to grow at a 7.8% CAGR, from INR 2,902 crore in 2023 to INR 4,227 crore in 2028, outperforming all markets except Indonesia, Kenya and Nigeria.

Trade magazines: This is a small segment, holding 3.1% of the B2B market. It is expected to grow at a 3.5% CAGR, from INR 263 crore in 2023 to INR 313 crore by 2028. Print advertising is expected to decline because readers will remain committed to physical editions as well as buying subscriptions to digital formats.

Seizing growth opportunities in a dynamic ecosystem

Consumers in South Africa, Kenya, and Nigeria reevaluated their discretionary spending on E&M products as a result of the sharp cost-of-living rises. Despite this, it is anticipated that all market sectors would have robust growth, with all markets outperforming Covid 2019 revenue levels.

Despite continued change and disruption, the industry reassessed its strategies, refocused on core operations and revised some key assumptions. Growth in South Africa’s E&M market stabilised in 2022, however this growth is still expected to outpace the global average. Nigeria is expected to experience the strongest growth in E&M revenue, with revenue expected to more than double from 2022 to 2027. Whilst newspapers, consumer magazines and books are forecast to continue to decline in South Africa and Nigeria, Kenya is forecast to achieve growth across all segments.

“International and domestic players alike are investing in local content and services to attract audiences and keep them engaged in an increasingly crowded landscape. The entertainment and media industry has always been a creative endeavour. In the coming years, armed with powerful technology, E&M leaders will have to be more creative about how they create, distribute and monetise products and services to achieve sustained growth.”

OTT platforms look to Africa as other markets slow down

There is significant room for growth within the African OTT video streaming market, with South Africa posting the highest OTT revenue on the continent. African streaming platforms have tailored themselves to African viewers with local content to compete with services that boast an established global footprint.

Growth in African OTT markets broadly outpaces the global average

Africa is home to rapidly expanding digital advertising markets

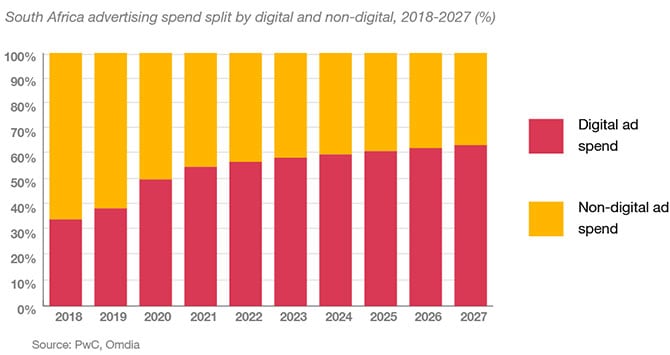

Digital has accounted for over half of advertising spend in South Africa since 2020, and by 2027, it is expected to take nearly two-thirds of ad spend. This broadly aligns with the global picture, where digital has led since 2019 and will account for 71.8% of ad spend in 2027.

Digital will account for nearly two-thirds of ad spend in South Africa in 2027

African gaming and esports to see future growth

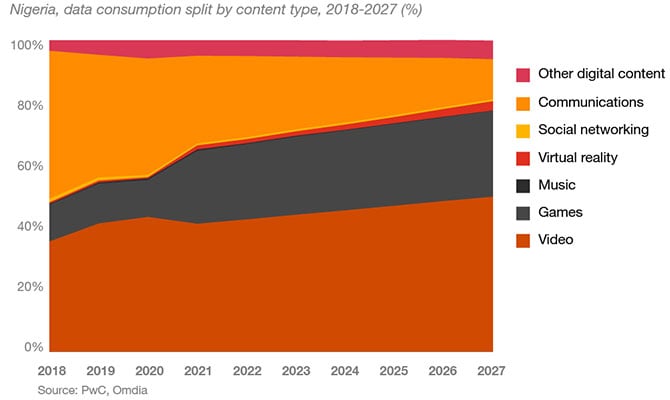

South Africa leads the three markets covered in terms of video games and esports revenue, with strong growth being recorded in 2022. This was especially prominent within the esports category, with total esports revenue up almost a third year-on-year. In Nigeria, games will overtake communications to become the second-largest category in terms of data consumption by the end of 2023, driven by a thriving mobile gaming landscape.

Games will overtake communications to be the second-largest content category by end-2023

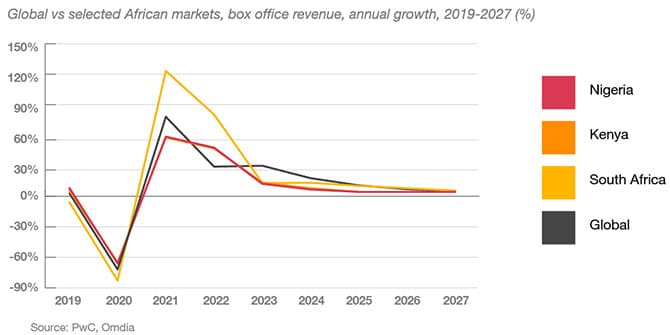

Live events and box-office continue their recovery

There has been a general rebound across the different categories of live events in South Africa, Nigeria and Kenya since the COVID-19 pandemic, with live music ticket sales performing strongly. Box office revenue has been recovering since 2021 but has yet to match pre-COVID-19 levels. South African cinema was the strongest performing of the three markets in 2022, with total revenue amounting to R862m.

South Africa is experiencing a strong rebound in box office revenue

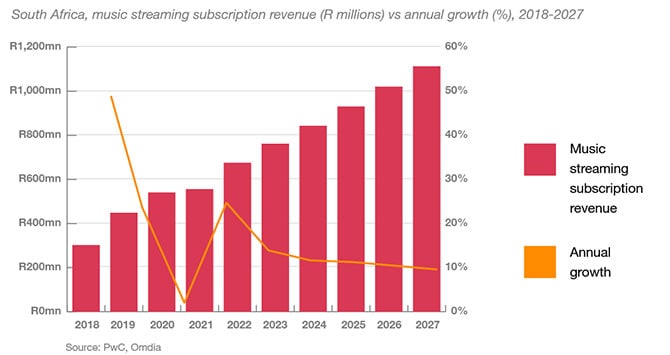

Music streaming adoption is rising

The music streaming market has never been stronger across South Africa, Nigeria and Kenya, with strong growth being experienced in music streaming subscription revenue. In South Africa, music streaming subscription revenue is set to rise at a 10.5% CAGR over the next five years to reach R1.1b in 2027.

Music streaming subscription revenue set to surpass R1.0b from 2026

Five-year projections of consumer and advertiser spending data across entertainment and media segments for South Africa, Kenya and Nigeria.

Understanding where consumers and advertisers are spending their money in the entertainment and media industry can help inform many important business decisions.

PwC’s Global Entertainment & Media Outlook provides a single comparable source of consumer and advertiser spending data and analysis. Updated annually, the intuitive online tool allows you to easily browse, compare and contrast spending and growth rates.

Take a tour of the Outlook data tool

Subscribers can sign up to access the full entertainment and media dataset, including:

Contact us for more information.